As brokers and agents well know, the real estate industry is complex, and there is always a risk of errors or omissions. That’s where E & O insurance comes in.

E&O insurance, short for errors and omissions insurance, is an insurance policy that provides coverage for professional liability claims resulting from mistakes, negligence, or omissions made by a broker or agent. This type of insurance is essential for real estate brokers, as the consequences of a claim can be financially devastating.

Real estate brokers might be responsible for managing rental properties, working with clients to buy or sell a home, and negotiating real estate transactions. In addition, real estate E&O insurance is often required by real estate franchises, and in some states, by law.

Despite best efforts, real estate brokers may face claims from clients due to a variety of factors. For example, a client may claim that the broker did not disclose important information about a property, or that the broker did not secure a lock box properly. Other claims could be related to mold, where a broker failed to detect or disclose a problem with the property.

E&O insurance provides real estate brokers with protection against such claims, covering legal defense costs and any damages awarded. This can help to minimize the financial impact of a claim and protect the reputation of the brokerage or agency.

Most real estate E and O policies have very broad exclusions for Contingent Bodily Injury & Property Damage (BI/PD). We dig into this into a lot more detail in our blog on why agents are exposed to BI/PD claims.

In short, this means that if someone is injured while you are showing a house, if an agent sells a home that has undisclosed mold and the buyer gets sick, or if a dog bites a buyer as they walk up to the front door with you, you probably have no E&O coverage!

This is especially true for property managers, but every single real estate agent has this exposure whether their E&O covers it or not. The Insurance Journal explains that this is an multi-industry insurance issue, making E&O insurance essential for coverage for an increasing number of bodily injury claims.

While some policies have coverage for BI/PD, most companies limit coverage extensively, or only cover up to a lower limit. You will often see coverage for bodily injury/property damage if the claim is at an open house or if the agent used a lock box.

The best of E&O policies provide full limits of coverage for a broad array of bodily injury or property damage claims.

The vast majority of real estate errors and omissions policies do not cover copyright, trademark, or TCPA (Telephone Consumer Protection Act) violations.

At FirmSecured, we work with a handful of insurance companies that will provide these coverages. As NAR details, copyright infringement on listing photos is not uncommon.

Many cyber insurance policies also often contain some coverages for copyright issues.

While almost all professional liability policies will cover defense costs, not all policies cover this in the same (or the best) way.

For example, some policies include defense costs within your limit of liability, meaning you will have less coverage to cover a settlement. Other E&O policies will provide a separate limit of coverage for defense costs.

You can learn more about how this difference can cost real estate brokers hundreds of thousands of dollars in our blog titled, “Defense Inside or Outside of the Limit?”

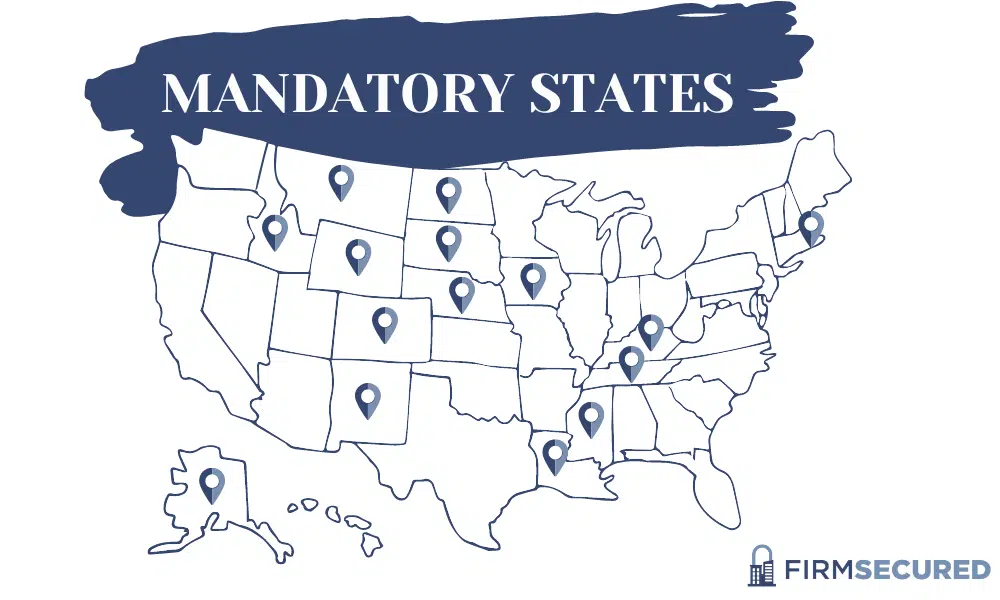

Here’s the current mandatory or required states for real estate errors & omissions (E&O):

Alaska, Colorado, Idaho, Iowa, Kentucky, Louisiana, Mississippi, Montana, Nebraska, New Mexico, North Dakota, Rhode Island, South Dakota, Tennessee, and Wyoming

An excess policy is not the same as the type of firm policy mentioned above. A true excess policy is like an umbrella policy, and it is excess to the primary, individual underlying policies. Firms often purchase an excess policy to meet franchise or contract requirements (typically $1 million limits).

The individual underlying policy is primary, meaning the individual policy’s entire policy limit is essentially a large “deductible” for the excess policy.

Our blog on best practices for renewing your individual E&O insurance explains a few things you should keep in mind when purchasing excess and individual policies.

Many real estate (and insurance) brokers prefer firm policies as they generally have much more robust coverage when compared to individual E&O policies.

As you can see in this graphic, for agencies that have a dozen or more agents, firm E&O is often much more cost-effective.

Switching from individual/excess policies to firm policies can seem daunting, so we wrote an article to help brokers in that transition.

Real estate E and O insurance policies are not designed to provide comprehensive coverage for cyber-related risks.

While some real estate E&O policies may offer a level of protection for certain cyber risks through an endorsement, add-on, or rider, the coverage is often limited. Typically, any coverage for cyber risks on an E&O policy is narrow in scope with lower limits of coverage. $25,000 -$100,000 limits on E&O policies for certain limited cyber claims is not too unusual.

So, if you are concerned about real estate cyber risks, especially third-party wire fraud, a separate or stand-alone cyber insurance policy is likely the best option for you. Traditionally, stand-alone cyber insurance policies will cover most claims up to $1 million, and generally cost significantly less than your E&O policy will.

For more information on cyber liability insurance for real estate brokers, check out our “Comprehensive Guide to Cyber Insurance for Real Estate Firms”.

As you can see, real estate E&O coverage has so many variables and nuances.

Many insurance agents have a broad generalized knowledge about commercial insurance, so they are simply not familiar with the specialized and unique aspects of real estate E and O coverage.

Be sure to work with an insurance agent who deals with real estate errors & omissions insurance policies every day. Find an insurance agent to represent you who not only has access to most of the E&O insurance programs available, but who will take the time to review your policy, compare/explain coverages, and present customized options for your firm.

If we have been a help to you in your E&O search, we would be honored with the opportunity to serve you and your team.