Embarking on the journey of real estate entrepreneurship? Wondering how much real estate E&O costs?

Whether you’re launching your own agency, stepping into the world of real estate as an agent, or setting out to conquer the market on your terms, you need real estate errors and omissions (E&O) insurance.

Asking How much is E&O coverage? What kind of E&O do I need? How do I buy it? are all natural questions as you purchase E&O for the first time.

Let’s dig into the details!

Average Real Estate E&O Rates

There are really two types of real estate E&O coverage, and your rate will depend on what type of coverage you have. Agents will either purchase individual E&O policies, or the brokerage will purchase firm-wide errors & omissions coverage. Let’s discuss each one separately.

Individual Real Estate E&O Cost

Individual E&O insurance policies typically range from anywhere from $100 to over $500 annually per agent depending on the state, insurance company, and what coverages are included.

Many individual policies have optional endorsement add-ons with coverages that you might need, such as bodily injury & property damage coverage, residential personal interest, or increased limits. These endorsements will affect the price of an individual E and O policy, but are often well-worth the extra cost.

That said, even with the extra endorsements, individual policies still might not be sufficient for the E&O needs of many brokers and agents. We discuss some of these considerations in our blog titled “Best practices when renewing with your individual E&O program.” Keep in mind, brokers might need to purchase a firm excess policy if agents have individual policy, resulting in increased costs for the brokerage. We break that down in our article comparing firm, individual, and excess policies.

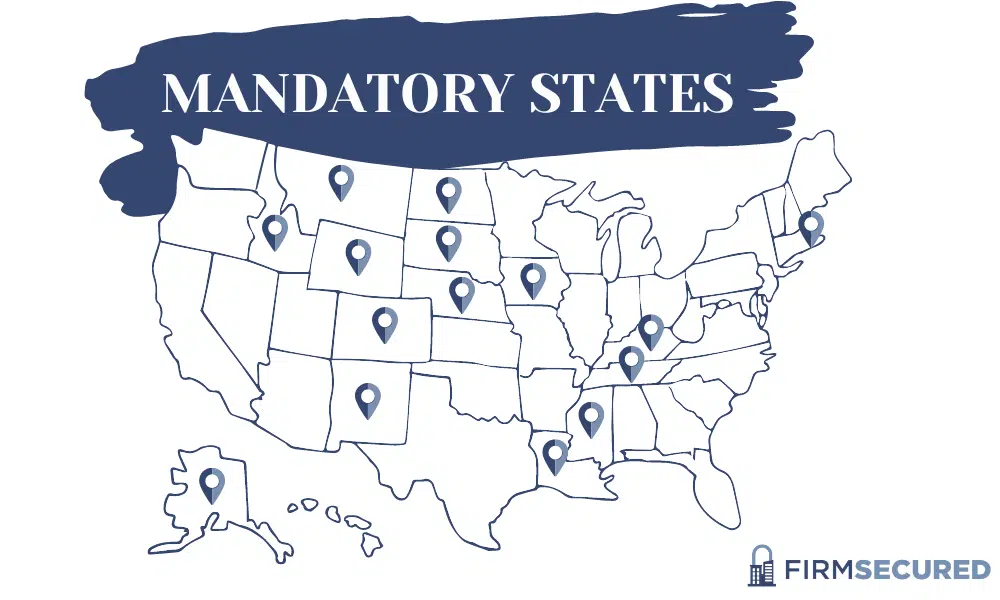

These individual policies are most common in mandatory states for real estate E&O (although by no means the only or best option for everyone in mandatory states). Those states are currently:

Firm Real Estate E&O Cost

A true real estate firm E&O insurance policy will cover not only the real estate brokerage’s legal entity, but also all brokers, agents, and independent contractors while doing business on behalf of the firm.

Typically, an underwriter will review a firm real estate E&O application. Your firm’s principal broker, owner, or office manager will answer questions related to your firm’s gross commission income (GCI), number of agents, risk management practices, along with other basic information about your firm.

For a new real estate agency projecting less than $1 million in GCI for their first year, a $1 million limit firm errors & omission policy will cost anywhere between $600-$2,000. Be careful though. Not all policies are the same, so you want to do your research to make sure you have the coverages you need.

For $1 million in E&O insurance coverage, a real estate firm with $1 million in revenue can expect to pay between $1,500 and $4,000 annually for E&O insurance. Firms with $5 million in revenue might pay anywhere from $7,000 to $15,000, while agencies bringing in around $10 million in revenue could pay anywhere between $15,000 and $30,000 for E&O insurance.

Brokerages doing over $100 million in GCI annually can expect to pay sometimes over $100k in E&O premium each year.

How E&O Prices are Determined

Generally, most firm E&O premiums are based primarily on a real estate agency’s annual gross commission income (GCI). An increase in revenue will generally correspond with an increase in premium at renewal.

Your past claims history is also a major factor that can influence the cost of E&O insurance. If you have had E&O incidents in the past, to an underwriter, this generally indicates that you are at a higher risk of future claims, leading to higher premiums.

If you are performing a higher percentage of often statistically higher risk transactions, your premium might change. Examples include firms reporting a high percentage of dual agency transitions, foreclosures, luxury or multi-million dollar homes, or the sale of agent-owned flips or properties developed/constructed by an agent.

Other factors that can impact the cost of E&O insurance include additional coverage endorsements, the specific type of real estate work you perform, and the state you are located in (especially since local real estate markets differ across the country).

Your policy’s deductible (retention) and your per occurrence and aggregate limits will impact your total price, as well as whether your defense costs are included inside or outside of the policy limit.

Of course, it is crucial to provide accurate information when applying for real estate errors & omissions insurance. Failure to provide accurate and complete information on an E and O application may lead to a denied claim, rescinding of coverage, or worse.

Is E&O Worth the Cost?

It’s important to remember that the cost of E&O insurance should be seen as an investment in the long-term stability of your agency (and agents). E&O claims can be very expensive, and budgeting a fraction of a percent of revenue each year for E&O can later be the difference between surviving a lawsuit and going out of business.

Some states mandate E&O coverage for real estate brokers, and most real estate franchises require that franchisees maintain professional liability coverage.

Finally, remember that E&O policies are not all the same. Companies offer very different coverages to real estate firms. Cutting corners on coverage for a cheap E and O price can cost you hundreds of thousands later on in the event of a denied claim.

Find an Independent Agent

When it comes to obtaining real estate E&O insurance, it is essential to work with an advisor who has expertise in both the real estate industry and insurance.

Find independent insurance agent you trust. They will have contracts and relationships with multiple insurance carriers to help you find the right coverage at the best rate.

Many generalized commercial insurance agents do not have a thorough understanding of the unique risks associated with the real estate industry, so it’s crucial to find an advisor who knows real estate E&O coverage well.

Get Options E&O Options

Our team would be honored with the opportunity to assist you or your firm with your E&O coverage. We work with real estate brokers nationwide on real estate insurance, and our goal is to help brokers not only find the best price, but also understand the coverages they are choosing.

To get started, simply complete the contact form below. If you would rather set up a few minutes to discuss your E & O coverage, you can schedule time on Google Meet here.

Finally, remember that most E&O policies do not cover some of the most common cyber liability claims for real estate brokers. So when budgeting for the cost of E&O, you might also want to start planning to budget for cyber insurance. We have a resource just like this one dedicated to explaining the cost of cyber insurance for real estate firms.